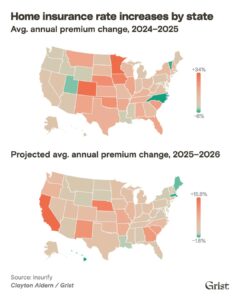

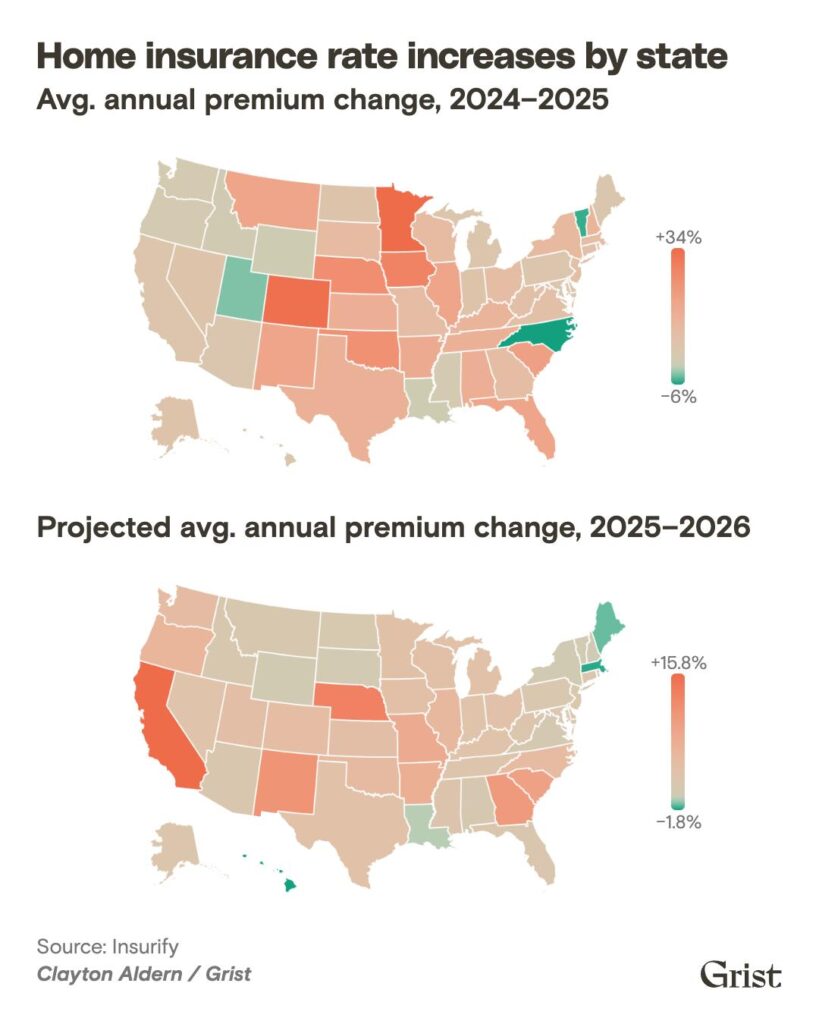

In recent years, as the United States has suffered a series of damaging climate disasters, experts have warned that the nation is headed toward a homeowner’s insurance crisis. Insurance companies dropped hundreds of thousands of customers who live in areas vulnerable to hurricanes and wildfires, and numerous small insurers have gone belly-up after big disasters. This has led some to forecast that a broader market failure in disaster-prone states is looming, or even a housing market collapse.

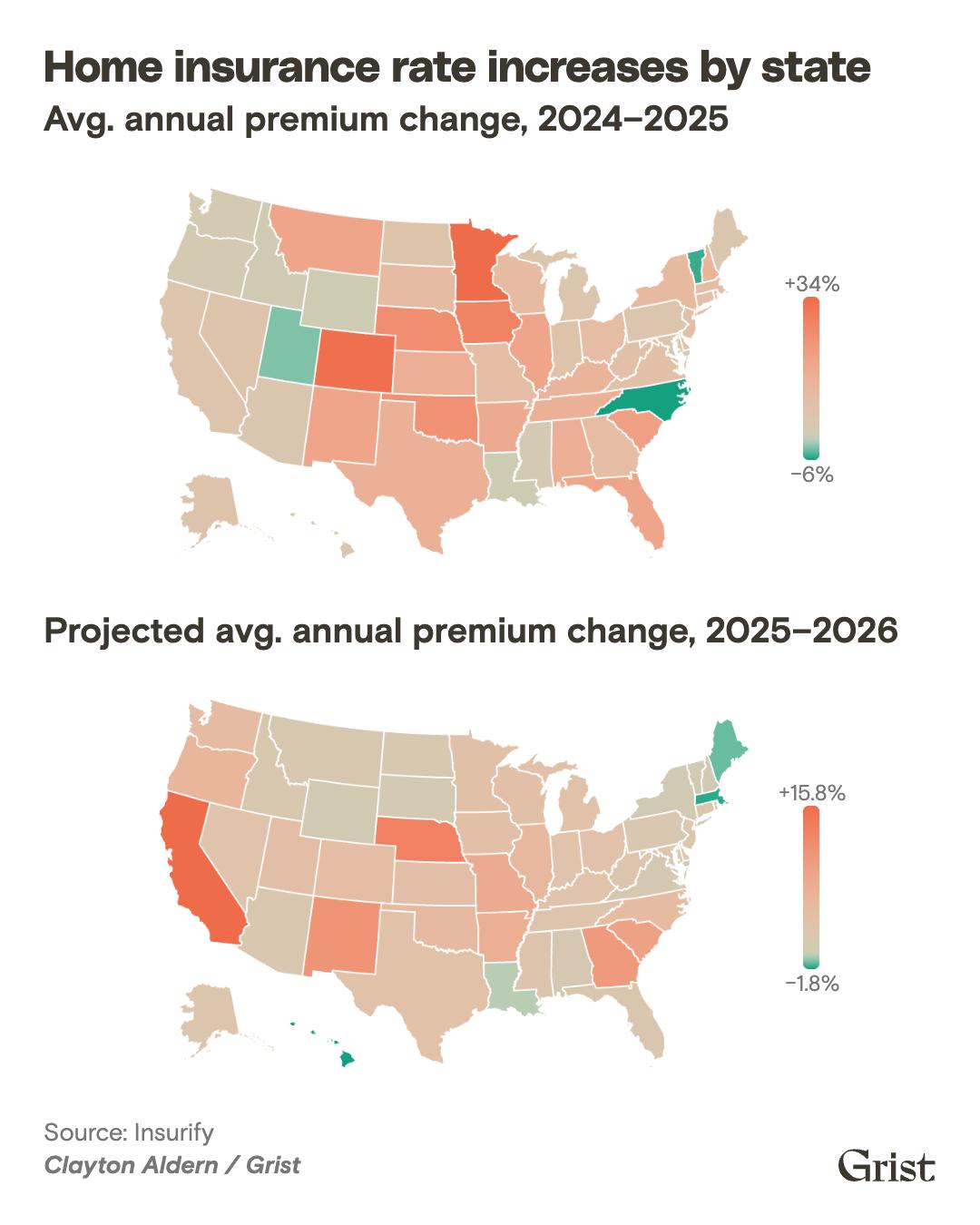

That has not happened yet. But in the meantime, insurance has gotten a lot more expensive — and the price hikes are not going anywhere. A new nationwide report from the insurance price comparison firm Insurify found that the average American homeowner’s insurance bill rose 12 percent last year, reaching $2,948 per year, and will rise another 4 percent this year. This is much faster than overall inflation for the same period. (These numbers don’t include flood insurance, which most often requires a separate plan, backed by the federal government.)

There are a lot of factors behind these rising bills: Insurance companies consider the value of a home, the cost of the materials needed to rebuild it, and even the credit scores of the homeowner. But the primary culprits are the rising toll of extreme weather as the planet warms and the millions of new homes developers have built in vulnerable areas. Insured losses from natural catastrophes in the U.S. averaged $100 billion a year between 2023 and 2025, up from an annual average of around $15 billion per year a decade earlier, according to the Insurance Information Institute.

Home insurance rate increases by state

Change in average annual premium